Lease vs. Buy Luxury SUV: Comprehensive Calculator Guide

Deciding between leasing and buying a luxury SUV is a pivotal financial choice for many discerning consumers. This decision requires a deep understanding of immediate expenses and long-term implications, making a robust lease vs buy luxury SUV calculator an indispensable tool.

Luxury vehicles come with unique financial considerations, including rapid depreciation and premium maintenance costs, which significantly influence the optimal choice. This guide will meticulously explore both acquisition paths, detailing their mechanisms and how a specialized calculator can illuminate the most advantageous financial route for your individual circumstances.

The Allure and Financial Realities of Luxury SUVs

Luxury SUVs captivate buyers with their exquisite blend of prestige, powerful performance, advanced comfort features, and cutting-edge technology. These vehicles often showcase superior craftsmanship, state-of-the-art infotainment systems, and high-performance engines, thereby justifying their elevated price points.

However, the premium nature of luxury SUVs also introduces distinct financial dynamics, particularly concerning their depreciation rates and ongoing operating costs. A truly informed decision mandates a clear grasp of these factors, as their impact varies significantly between leasing and outright purchasing.

Understanding Luxury SUV Leasing: The Contractual Journey

Leasing a luxury SUV essentially functions as a long-term rental agreement, where you pay for the estimated depreciation of the vehicle over a specified lease term, augmented by finance charges. This arrangement enables individuals to drive a brand-new, high-end vehicle without the enduring commitment of full ownership.

Crucial terms in a lease agreement include the ‘money factor,’ which is analogous to an interest rate, and the ‘residual value,’ representing the projected market value of the vehicle at the lease’s conclusion. Grasping these core components is fundamental for accurately assessing the true total cost of any lease agreement.

Advantages of Leasing a Luxury SUV

Leasing offers several compelling benefits that appeal to many luxury SUV enthusiasts. It provides financial flexibility and access to the latest models without the long-term commitment of ownership.

- Lower Monthly Payments: Lease payments are typically significantly lower than loan payments for an equivalent vehicle because you are only financing the depreciation, not the entire purchase price. This makes driving a more expensive luxury model highly accessible within a manageable monthly budget.

- Always Drive a New Car: Leasing cycles often align perfectly with new model releases, allowing you to regularly upgrade to the latest luxury SUV equipped with cutting-edge features and technology. This ensures you consistently drive a vehicle under warranty, minimizing concerns about significant long-term maintenance issues.

- Reduced Maintenance Costs: Most lease terms fall comfortably within the manufacturer’s original warranty period, meaning that major repairs are generally covered, offering considerable peace of mind. This proactively helps avoid unexpected and often exorbitant expenses commonly associated with older luxury vehicles.

- Potential Tax Advantages for Businesses: For eligible businesses, lease payments can often be partially or entirely tax-deductible, presenting a valuable potential financial benefit. It is always prudent and highly recommended to consult with a qualified tax professional to understand the precise implications for your specific business.

Disadvantages of Leasing a Luxury SUV

Despite its advantages, leasing a luxury SUV comes with notable drawbacks that can significantly impact long-term financial outcomes and personal freedom. Understanding these limitations is crucial before committing to a lease.

- No Equity or Ownership: At the conclusion of a lease, you do not own the vehicle and have accumulated absolutely no equity, unlike buying where payments contribute to an appreciating (or depreciating) asset. This means you will have no vehicle to sell or trade in the future, representing a complete expenditure.

- Strict Mileage Restrictions: Lease agreements impose stringent annual mileage limits, typically ranging from 10,000 to 15,000 miles, with severe per-mile penalties for exceeding these caps. This can be a substantial deterrent and financial burden for individuals who drive extensively or unpredictably.

- Wear and Tear Charges: Beyond normal wear, any excessive damage, interior wear, or unauthorized modifications to the vehicle will result in significant fees upon lease return. Maintaining the luxury SUV in impeccable condition is therefore paramount to avoid these costly charges.

- Limited Customization: Since you do not technically own the car, major modifications or permanent alterations are generally prohibited by the lease agreement. This severely restricts your ability to personalize the vehicle beyond factory-installed options.

Understanding Luxury SUV Buying: The Path to Ownership

Buying a luxury SUV signifies acquiring complete and outright ownership of the vehicle, a transaction typically financed through a dedicated automotive loan rather than an upfront cash payment. This option provides the purchaser with unparalleled freedom and unencumbered control over their vehicle from the very moment of acquisition.

When you opt to buy, you assume responsibility for the entire purchase price, which is customarily amortized over a loan term spanning several years with accrued interest. The specific loan structure, the size of your initial down payment, and the prevailing interest rate are all pivotal factors that profoundly influence your overall total cost of ownership and subsequent monthly financial outlays.

Advantages of Buying a Luxury SUV

Buying a luxury SUV offers a distinct set of benefits focused on long-term ownership, flexibility, and financial asset building. These advantages resonate strongly with those seeking permanence and control over their vehicle.

- Full Ownership and Equity: As an owner, you steadily build equity with each loan payment made, and the vehicle itself becomes a tangible asset that you can confidently sell or trade in the future. This provides a genuine financial return on your investment, even when accounting for depreciation.

- No Mileage Restrictions: Purchasing a vehicle completely removes any limitations on how much you can drive, offering absolute freedom for extensive road trips, daily commutes, or prolonged travel. This is an undeniable and crucial advantage for individuals with high annual mileage requirements.

- Complete Customization Freedom: Ownership grants you the absolute liberty to extensively personalize your luxury SUV with any desired modifications, aftermarket accessories, or aesthetic changes, without any concerns about contractual violations. This enables you to truly tailor the vehicle to your unique tastes and functional needs.

- Potential for Long-Term Savings: After successfully paying off the entire loan, you effectively eliminate all monthly car payments, leading to substantial long-term financial savings. This period of ownership without debt can significantly offset the initial higher costs, particularly for those who retain their vehicles for extended periods.

Disadvantages of Buying a Luxury SUV

While buying provides ownership, it also comes with significant financial responsibilities and risks, particularly concerning depreciation and maintenance. These factors warrant careful consideration before making a purchase.

- Higher Monthly Payments: Loan payments are generally higher than lease payments because you are financing the entire purchase price of the vehicle, not just its depreciation. This can place considerable strain on monthly budgets, especially when acquiring premium luxury models.

- Direct Depreciation Risk: Luxury SUVs are often susceptible to rapid and significant depreciation, particularly during their first few years of ownership, meaning the vehicle’s market value can drop considerably. This substantial loss in value is directly and entirely borne by the owner.

- Increased Maintenance and Repair Costs: Once the manufacturer’s original warranty expires, you become solely responsible for all maintenance and repair expenses, which can be extraordinarily substantial for complex luxury vehicles. These unforeseen costs can accumulate very quickly and are often difficult to budget for accurately.

- Resale Hassle: The process of selling a used luxury SUV can frequently prove to be a time-consuming, complex, and often challenging endeavor. Successfully finding the right buyer and negotiating a fair market price demands both considerable effort and a comprehensive understanding of the current automotive market.

Demystifying the Lease vs. Buy Luxury SUV Calculator

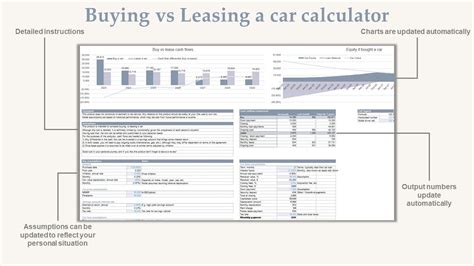

A specialized lease vs buy luxury SUV calculator is meticulously engineered to provide a precise, side-by-side comparison of the intricate financial implications inherent in each acquisition option. This indispensable digital tool typically necessitates several key inputs to generate highly accurate financial projections, thereby enabling a clear visualization of the true monetary cost over a chosen timeframe.

These essential inputs commonly encompass the vehicle’s Manufacturer’s Suggested Retail Price (MSRP), your intended down payment amount, prevailing loan interest rates, the lease’s specific money factor, the projected residual value, and your desired lease and loan terms. The calculator then diligently processes these diverse figures to present a comprehensive snapshot of total expenditures, precise monthly payments, and anticipated future equity, empowering you to make a profoundly informed and data-driven decision.

Essential Inputs for Your Calculator

To ensure the most accurate results from any lease vs. buy calculator, inputting correct and complete data is paramount. Each piece of information plays a vital role in the financial projections.

- Vehicle MSRP: This is the manufacturer’s suggested retail price, serving as the baseline for calculations, even if you negotiate a lower actual purchase price. It establishes the foundation for depreciation and financing estimates.

- Down Payment: Your initial lump sum cash contribution directly reduces the amount that needs to be financed for both buying and leasing scenarios. A larger down payment can significantly lower monthly payments or total interest paid.

- Loan Interest Rate (APR): For buying, this is the annual percentage rate applied to your car loan, directly influencing the total interest accrued over the loan’s duration. It is crucial for understanding your long-term financial commitment.

- Lease Money Factor: Often presented as a small decimal (e.g., 0.00200), this acts as the equivalent of an interest rate within a lease agreement. It is critical for calculating the finance charge component of your monthly lease payment.

- Residual Value: This is the estimated market worth of the car at the conclusion of the lease term, expressed as a percentage of the original MSRP. A higher residual value typically translates into lower monthly lease payments, as less depreciation is financed.

- Trade-In Value: If you possess an existing vehicle, its trade-in value can effectively reduce your out-of-pocket expenses for the new luxury SUV. This credit is applicable whether you choose to buy or, in many cases, can be applied as an upfront payment towards a lease.

- Sales Tax: Sales tax varies by region and applies differently to leases versus purchases. Some jurisdictions tax the full purchase price when buying, while others tax only the monthly lease payments, creating crucial cost distinctions.

- Term Length: This specifies the duration of either the lease or loan agreement, typically expressed in months (e.g., 36, 48, 60 months). Longer terms often mean lower monthly payments but invariably lead to higher total interest paid over the entire period.

- Annual Mileage: For leasing, your estimated yearly mileage is a critical input, as lease agreements enforce strict limits. Accurately forecasting your driving habits is essential to meticulously avoid costly over-mileage penalties.

Crucial Financial Metrics Beyond Monthly Payments

Beyond merely comparing monthly payments, a comprehensive financial evaluation necessitates assessing several critical metrics when deciding between leasing and buying. A sophisticated calculator will meticulously highlight these figures, facilitating a much deeper comprehension of the overall financial commitment involved.

Grasping metrics such as the total cost of ownership, net present value, and potential equity allows you to forge a decision perfectly aligned with your overarching long-term financial aspirations. Overlooking these profound financial insights can unfortunately lead to unexpected expenditures or foregone opportunities.

Total Cost of Ownership (TCO)

The Total Cost of Ownership (TCO) stands as perhaps the most vital metric, encompassing all direct and indirect expenses associated with the luxury SUV over a defined period. This includes the purchase price or aggregate lease payments, all accumulated interest, relevant taxes, insurance premiums, fuel costs, routine maintenance, unforeseen repairs, and the significant impact of depreciation or lost equity.

A calculator proficiently projects the TCO for both leasing and buying options, thereby delivering a truly holistic financial comparison rather than fixating solely on monthly outlays. This all-encompassing perspective ensures that you account for every potential expenditure, both explicit and implicit.

Equity and Future Value Considerations

When you choose to buy, each loan payment incrementally contributes to building equity in the vehicle, which then possesses a tangible future resale or trade-in value. This accrued equity represents a distinct financial asset, though its value is continuously offset by the relentless force of depreciation, particularly prominent in luxury vehicles.

Leasing, conversely, offers no direct equity accumulation, but it simultaneously liberates you from the personal burden and effort involved in selling a potentially depreciated asset. The calculator can graphically illustrate the projected equity for buyers versus the complete absence of equity for lessees, clarifying this fundamental difference.

Tax Implications and Financial Planning

The tax treatment pertaining to vehicle leases versus outright purchases can exhibit considerable variation, contingent upon your specific geographical location and whether the vehicle is designated for personal or legitimate business use. For instance, some jurisdictions impose sales tax on the entire purchase price of a financed vehicle, while others levy it solely on the monthly lease payments, creating significant cost disparities.

While a proficient calculator will incorporate basic sales tax differentials, it is invariably advisable to consult with a qualified tax advisor to fully comprehend and navigate these complex nuances. Understanding these intricate tax distinctions can unveil unexpected hidden costs or fortuitous savings opportunities.

Personal Factors Beyond the Financial Calculator

While a calculator furnishes invaluable financial data, your unique personal circumstances and individual preferences hold equally critical sway in the ultimate lease vs. buy decision. These influential non-financial factors frequently tip the scales in one direction or another, meticulously aligning the chosen acquisition method with your distinct lifestyle and priorities.

It is paramount to thoroughly assess your personal financial stability, typical driving habits, and overarching long-term vehicle ownership goals before committing to a final decision. A choice predicated solely on numerical analysis might regrettably overlook crucial practical considerations that profoundly impact your satisfaction and overall well-being.

- Your Financial Situation: Critically evaluate your current cash flow, accumulated savings, and overall financial stability. Can you comfortably accommodate potentially higher monthly payments or a substantial initial down payment for buying, or would the more modest monthly outlay of leasing better suit your existing budgetary constraints?

- Driving Habits and Annual Mileage: If your driving patterns consistently involve significantly above-average mileage (e.g., exceeding 15,000 miles per year), then buying is demonstrably the more economically prudent choice due to severe penalties associated with lease mileage overages. Conversely, individuals with consistently low annual mileage may discover leasing to be a considerably more appealing option.

- Desire for New Technology and Features: For those who frequently crave the very latest models replete with cutting-edge technology and advanced safety features, leasing provides an ideal pathway for regular vehicle upgrades. Buyers typically retain their vehicles for longer durations, thereby potentially missing out on immediate access to the newest automotive innovations.

- Vehicle Customization Needs: Outright ownership grants buyers absolute freedom to extensively personalize their luxury SUV with various aftermarket parts, accessories, or bespoke modifications. Lease agreements, however, generally prohibit significant alterations, mandating that the vehicle be returned in its original, unmodified factory condition.

- Long-Term vs. Short-Term Ownership Goals: If your intention is to retain a vehicle for many years, ideally well beyond the loan repayment period, then buying represents the unequivocally superior choice. Conversely, if you relish the experience of driving a new car every few years without the inherent hassles of private selling, leasing will likely prove to be a far better fit.

- Tolerance for Maintenance and Repair Risks: With an outright purchase, particularly once the original factory warranty has expired, you bear the full and often substantial burden of all maintenance and repair costs. Leasing frequently provides coverage within the warranty period, thereby significantly mitigating these unpredictable and potentially hefty expenses.

When to Lease vs. When to Buy: Practical Scenarios

The optimal choice between leasing and buying a luxury SUV is intrinsically individualistic, profoundly contingent upon specific personal situations and prevailing priorities. There exists no universally ‘better’ option; instead, the superior choice is invariably the one that best suits your unique circumstances and financial objectives.

By carefully considering which of these common profiles most closely aligns with your own, you can gain a much clearer understanding of the practical implications inherent in each financing method. This vital contextual understanding expertly complements the raw financial data, leading to a more personalized, effective, and ultimately satisfying decision.

Consider Leasing If:

- You prioritize significantly lower monthly payments, desiring to drive a higher-end luxury SUV than you could realistically afford to purchase outright.

- You enjoy driving a new car every 2-4 years, consistently experiencing the latest automotive technology, advanced safety features, and contemporary styling.

- Your annual driving mileage is consistently low, typically falling well within specified limits such as under 12,000 to 15,000 miles per year.

- You strongly prefer minimal maintenance hassles and desire to consistently operate your vehicle within its manufacturer’s warranty periods.

- You are averse to the long-term commitment of vehicle ownership or wish to avoid the often-cumbersome burden and time-consuming process of selling a used car yourself.

Consider Buying If:

- You definitively plan to retain the luxury SUV for an extended period, ideally well beyond the initial loan payoff period, maximizing your long-term investment.

- You anticipate driving a substantial amount annually, meaning you would inevitably exceed the typical mileage limitations imposed by lease agreements.

- You deeply value outright vehicle ownership, the tangible process of building equity, and the security of possessing a valuable asset for the long term.

- You desire the complete freedom to extensively customize your luxury SUV with personalized modifications or accessories without any contractual restrictions.

- You possess a comfortable level of financial preparedness to confidently handle all maintenance and potentially substantial repair costs once the manufacturer’s warranty eventually expires.

- You are financially capable of comfortably affording the inherently higher monthly payments associated with a car loan or can make a substantial initial down payment.

Beyond the Calculator: Essential Final Considerations

While a sophisticated lease vs buy luxury SUV calculator serves as an indispensable analytical instrument, it represents merely one crucial component of the entire decision-making mosaic. A myriad of other practical considerations also warrant meticulous attention, collectively contributing to a truly holistic and well-rounded choice.

These additional elements, ranging from specific insurance implications to the evolving dynamics of the pre-owned luxury vehicle market, can profoundly influence your overall satisfaction and long-term financial outcome. It is always prudent to look beyond the immediate numerical figures and adopt a broader, more encompassing perspective.

Insurance Costs for Luxury SUVs

Luxury SUVs inherently command higher insurance premiums, irrespective of whether you opt to lease or buy them outright. However, leasing companies frequently mandate specific, often more comprehensive, insurance coverages than a buyer might independently choose, potentially escalating your monthly expenses.

It is absolutely critical to procure detailed insurance quotes for both potential scenarios before making any commitment to either leasing or buying. This proactive step ensures you accurately factor in the full monthly outlay, effectively preventing any unwelcome financial surprises post-agreement signing.

Maintenance and Warranty Coverage

Luxury vehicles are renowned for their intricate engineering and sophisticated components, which can unfortunately translate into extraordinarily expensive repair costs. While leasing typically keeps you comfortably within the manufacturer’s warranty period, outright ownership signifies that you will eventually bear full responsibility for these potentially significant expenses.

Prudently consider acquiring an extended warranty if you decide to buy, especially for a luxury SUV, to effectively mitigate future repair risks and provide financial protection. This additional cost can add to your upfront expenditures but offers invaluable long-term peace of mind.

Future Market Value and Depreciation Realities

Luxury SUVs are notoriously susceptible to significant depreciation, particularly pronounced during their initial years of ownership. While buyers directly absorb this considerable loss in value, lessees indirectly finance it through higher money factors or lower residual values embedded within their agreements.

Thoroughly researching the specific luxury SUV model’s historical depreciation rates can yield invaluable insights into its projected future worth. This crucial information enables you to meticulously fine-tune your calculator inputs and cultivate realistic expectations regarding the vehicle’s long-term market value.

Making Your Confident, Informed Decision

The ultimate choice between leasing and buying a luxury SUV is an inherently personal one, intricately shaped by a harmonious blend of astute financial prudence and individual lifestyle preferences. There exists no singular, universally ‘better’ option; instead, the optimal choice is undeniably the one that perfectly aligns with your unique circumstances and aspirations.

Leverage a robust lease vs buy luxury SUV calculator as your foundational analytical tool, but critically augment its invaluable insights with a thoughtful and candid assessment of your personal driving habits, overarching financial goals, and fundamental desire for vehicle ownership. By adopting this comprehensive and balanced approach, you can confidently navigate this significant financial decision, ultimately enjoying your luxury SUV with the absolute assurance that you have made the smartest and most suitable choice for yourself.

Frequently Asked Questions (FAQ)

What is the primary financial difference between leasing and buying a luxury SUV?

The primary financial difference lies in ownership and what you pay for. When leasing, you primarily pay for the vehicle’s depreciation over the lease term, plus a money factor (interest equivalent), and you never own the car. When buying, you pay for the entire purchase price of the vehicle, either upfront or through a loan, building equity over time.

What key terms should I understand when considering a luxury SUV lease?

For a luxury SUV lease, understanding the ‘money factor’ (which dictates the finance charge), the ‘residual value’ (the vehicle’s projected value at lease end), and annual ‘mileage limits’ is crucial. These terms directly impact your monthly payments and potential end-of-lease costs.

How does depreciation uniquely affect luxury SUVs in the lease vs. buy decision?

Luxury SUVs often experience higher and more rapid depreciation compared to standard vehicles, especially in the initial years. When leasing, this depreciation is factored into your payments; when buying, you directly absorb this loss in asset value, which can significantly impact your equity and resale value.

When is a lease vs. buy calculator most beneficial for luxury SUVs?

A lease vs. buy calculator is most beneficial when you need a detailed, side-by-side financial comparison of both options, especially given the high costs and complex financial terms of luxury SUVs. It helps visualize total cost of ownership, monthly payments, and long-term equity, allowing for an informed decision tailored to your specific financial situation and driving habits.

Can I customize a luxury SUV if I choose to lease it?

Generally, no, significant customization is not allowed when leasing a luxury SUV. Lease agreements typically require the vehicle to be returned in its original, unmodified condition (aside from normal wear and tear). Buyers, on the other hand, have full freedom to customize their owned vehicle.